Open Banking Payments can be a great way to save money on payment processing costs. Typically, credit card processing fees range from 2-5% depending on the company you use.

Moreover, you usually don’t get access to your money instantly.

With open banking you can pay as little as 0.5% per transaction and get your money instantly.

Below we look at the 9 best open banking payment providers in the UK.

| Company | Standard Transaction Fee | Free Trial? |

|---|---|---|

| bopp | 0.5% (max 50p) | Yes, 30 days |

| Ordo | 20p + VAT | Yes |

| Nuapay | Not stated | Not Stated |

| Token Payments | Not stated | Not Stated |

| Tink | Not stated | Not Stated |

| Modulr | Not stated | Not Stated |

| Volt | Not stated | Not Stated |

| Truelayer | Not stated | Not Stated |

| Vyne | Not stated | Not Stated |

The rankings below are in no particular order.

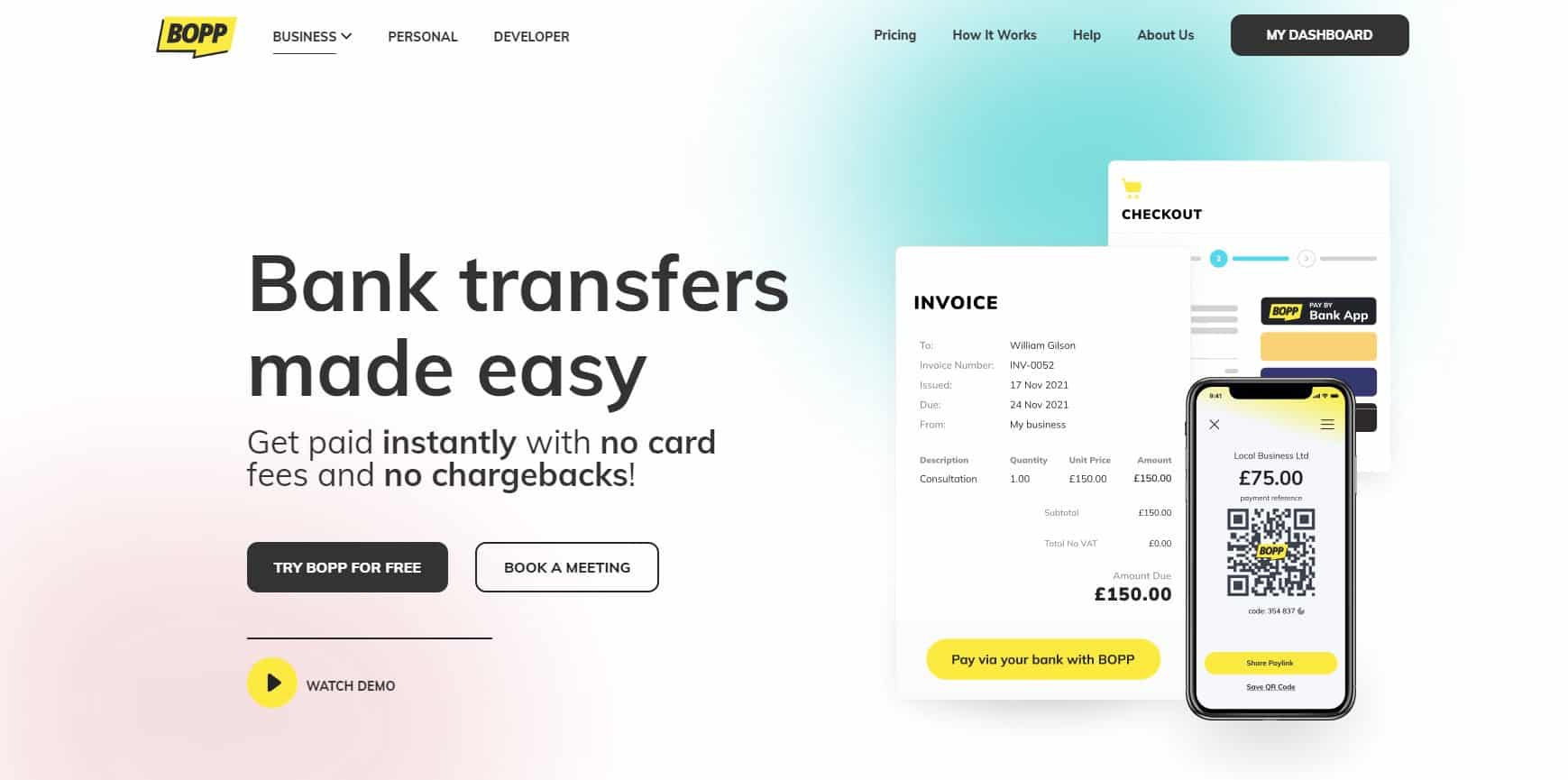

1. bopp

bopp pricing and features:

- Pay as you go plan offers 0.5% Transaction fees (5p minimum/50p maximum fee per transaction)

- Free starter plan (limit £100 per month)

- Value plan lets you pay just £10/month to process up to £5,000 worth of payments.

- 30-Day Free Trial

- No Cancellation Fees, No Minimum Term, No Hidden Fees

- Securely accept payments online without requesting debit or credit card information

- Digital mobile point of sale (mPOS) payments without a card reader

- Easily add BOPP to any other third party applications, no coding required

- Remove card processing fees and the PCI risks of mail order telephone order payments

- Make your invoices easy to pay. Easy one time set up

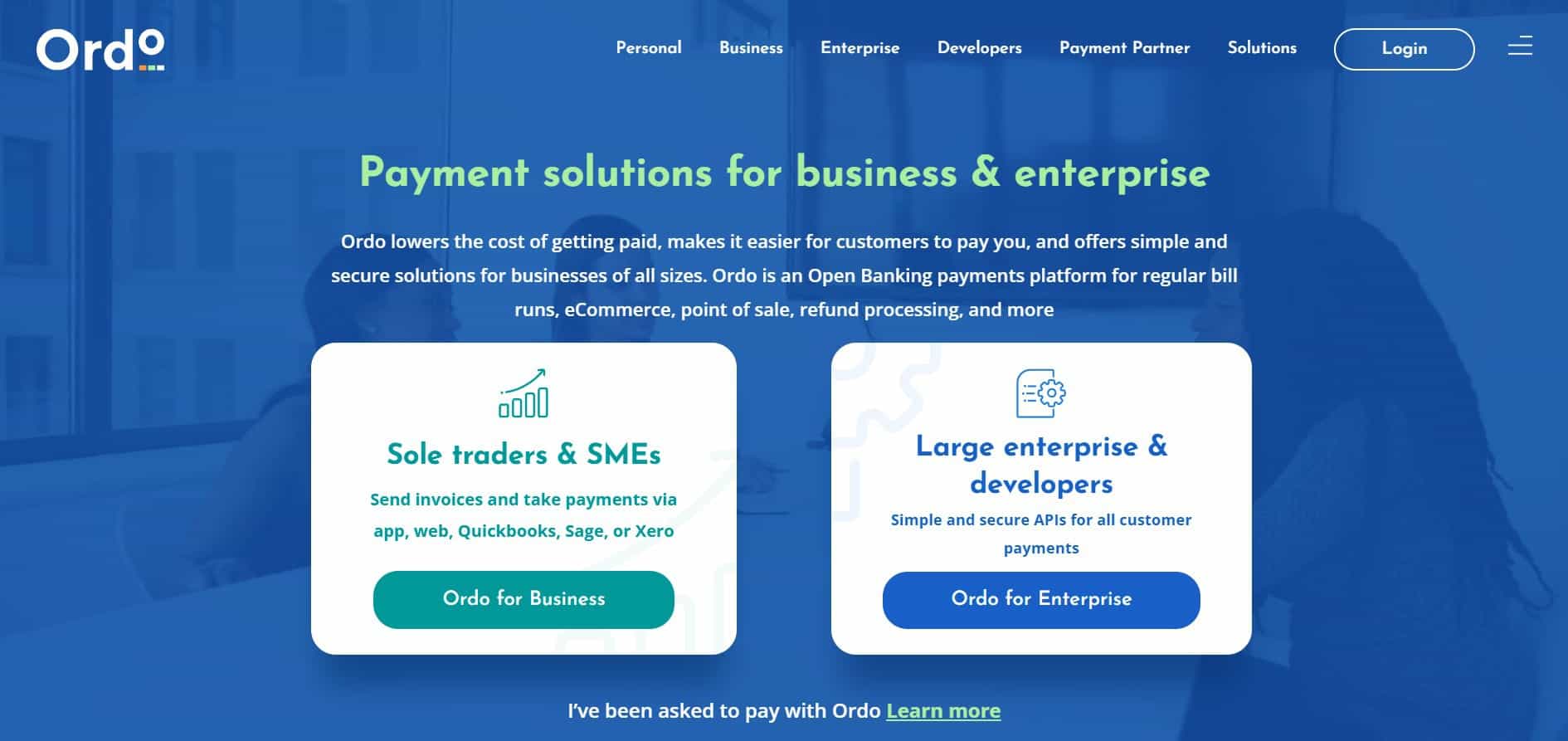

2. Ordo

Ordo pricing and features:

- Only pay 20p + VAT per transaction

- Free signup with no setup fees or contracts

- Offer a white-labelled ‘Pay Now’ button for websites

- No card details to enter, no security codes, no chargeback risk

- Facilitate refunds using the same open banking technology to return payments

- Ability to send secure payment tokenised links or QR codes in an email or message

- No need for bespoke secure telephony solutions to capture and secure card details

- Securely send invoices with embeded payment links

- Point of Sale solutions using QR codes

- Offer variable recurring payment (VRP) solutions

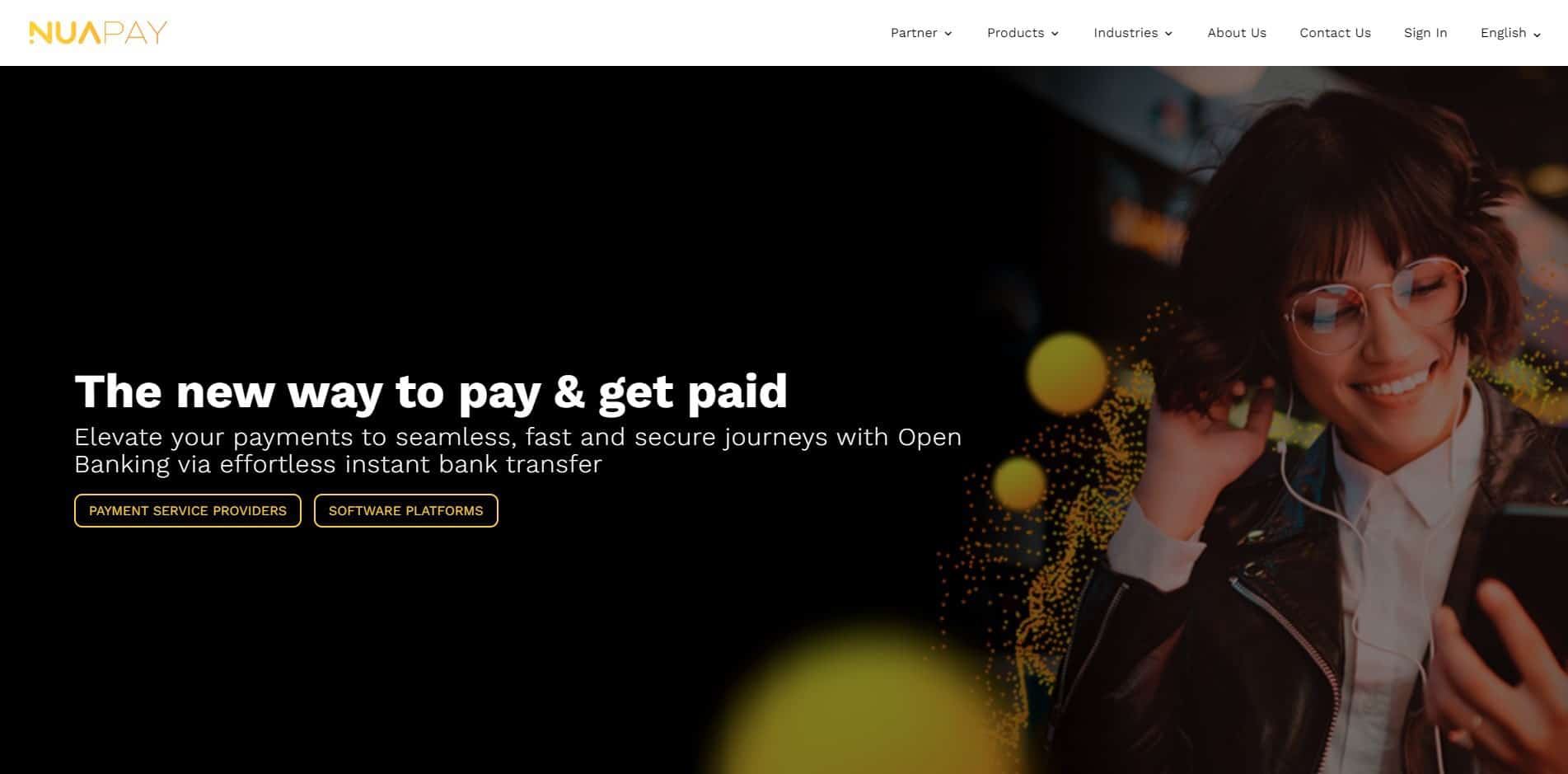

3. Nuapay

Nuapay pricing and features:

- One, simple, low-cost fee

- No charges on failed or declined transactions

- No chargebacks

- Fast and simple customer checkout with no card details to enter

- Merchant receives money (and sends refunds) in real-time

- Instalment plans & recurring payments with one click

- Real-time webhooks to confirm payment status

- Fully SCA compliant payment method, lowering your fraud rates

- Consumers connect securely to their internet or mobile banking to make a payment

- No credentials or account details disclosed to merchant, so no PCI DSS requirements

4. Token Payments

Token Payments pricing and features:

- 2-20X lower cost than traditional payment methods

- Instant Settlement

- Operate in 16 markets across Europe covering 80% of bank accounts

- High payment success rates

- Process 30 million payments annually

- Offers brandable solutions

- Ability to process standing orders and variable recurring payments

- Ecommerce and POS options available

- QR codes and pay by link options

- Offers a range of reporting tools

5. Tink

Tink pricing and features:

- Accept payments in real time

- Streamline user experiences

- Cut costs and fight fraud without extra work

- Simple bank payments that can be embedded anywhere – in-app, online or as a QR code.

- Offer Pay by Bank on ecommerce websites

- Fraud and chargebacks kept to a minimum

- Takes less than 40 seconds per payment

- 80-90% of customers complete payments once they start

- Up to 80% cheaper than other payment methods

- 6,000+ Connections to all major banks across Europe in 18 countries

6. Modulr

Modulr pricing and features:

- Modulr combines Open Banking payments with e-money accounts

- Pre-fill payment details

- Redirect customers to their banking apps while keeping them within your brand

- Instantly notify them when funds arrive

- No more expensive card processing fees

- No more chargebacks and chargeback fees

- No more having to input long card numbers, expiry dates or CVV codes

- No more middlemen and waiting days for settlement

- Easily create Open Banking Standing Order

- Collect up to £250,000 with single immediate payments

7. Volt

Volt pricing and features:

- Unified commerce experience

- Optimised for QR

- Ability to host on your website

- Data-driven optimisation

- Intelligent bank search

- Ability to use your own brand name

- Fewer fraud costs: account-to-account (A2A) payments are inherently more secure than card payments

- Seamlessly expand into new markets

- Use their super gateway via API

- Pay by Link enables shoppers to buy where and when they want

8. Truelayer

Truelayer pricing and features:

- Reduce friction, fight fraud and cut costs with open banking payments

- Let your customers make payments via multiple channels, including text, email, social or in-store

- Payments for crypto and web3

- Offers variable recurring payments

- Pre-populated payment details

- App-to-app flows

- Users authenticate every payment with their bank, reducing the risk of fraud and unauthorised transactions

- Convert more customers by streamlining onboarding with a single payment

- Ensure new signups turn into active users by combining the sign-up process with an initial deposit

- Solutions for high risk industries like travel, financial services, iGaming and cryptocurrencies.

9. Vyne

Vyne pricing and features:

- 96% acceptance rate

- Integrate in as little as 2 days

- Funds arrive in seconds and you can save up to 80% on transaction fees

- Instant settlements, refunds and payouts

- Less card fraud and chargebacks by taking seamless, SCA embedded account-to-account (A2A) payments

- 99% UK and 95% European bank coverage

- Pay by link and QR codes

- Pay online, in-store or in-app

- Hosted or direct integration

- Offers 3 different tiers

Open Banking Payments FAQ

What are open banking payments?

Open banking payments, also sometimes referred to as account-to-account (A2A) payments allow customers to pay using their bank account rather than a credit or debit card.

Open baking payments can be enabled for all types of transactions including online, in-app, over the phone and even in-person.

You can learn more at the Open Banking website.

How do open banking payments work?

There are a variety of different implementations depending on where you’re accepting payments.

For online and app payments there hosted checkout solutions that allow users to pay directly using their bank’s app or online account.

For in-person payments either a QR code or payment link can be used to pay via invoice or at the point of sale again by connecting to their bank’s app.

Phone payments can also be completed by QR code or payment link but this has to be sent to the customer either via email, SMS or WhatsApp.

What are the benefits of open banking payments?

Here are just some of the benefits of open banking payments vs traditional card payments:

1. Lower transaction fees

Many providers claim to be up to 80% cheaper than competing card processing options.

2. Lower refund and chargeback rates

Customers have to verify their identity with their bank before payment. This reduces the chances of customers asking for a refund or chargeback. And also reduces the chances of someone paying via a stolen card.

3. Get your money instantly

As soon as your customer pays the money is in your bank account. No more waiting up to 5 business days to get the money from your merchant account.

4. Lower regulatory burden

No need for PCI-DSS compliance when using open banking.

5. Ability to integrate with existing payment infrastructure

Most open banking payment solutions work alongside your current payment flow. It just acts as one additional, low-cost payment option which should in theory help improve conversion rates.