Wondering who’s currently paying the highest interest rates on business savings accounts in the UK? Below we compare the 33 best business savings accounts to find out which bank is paying the most and which one’s are paying the least.

The table below compares interest rates offered by leading banks.

But be aware many banks have restrictions on how much you need to deposit to actually open an account. We do our best to outline these restrictions below:

| Min Instant Access Interest Rate (AER) | Max Instant Access Interest Rate (AER) | |

|---|---|---|

| Tide* | 3.35% | 4.00% |

| Kent Reliance | 3.81% | 3.81% |

| United Trust Bank | 3.50% | 3.80% |

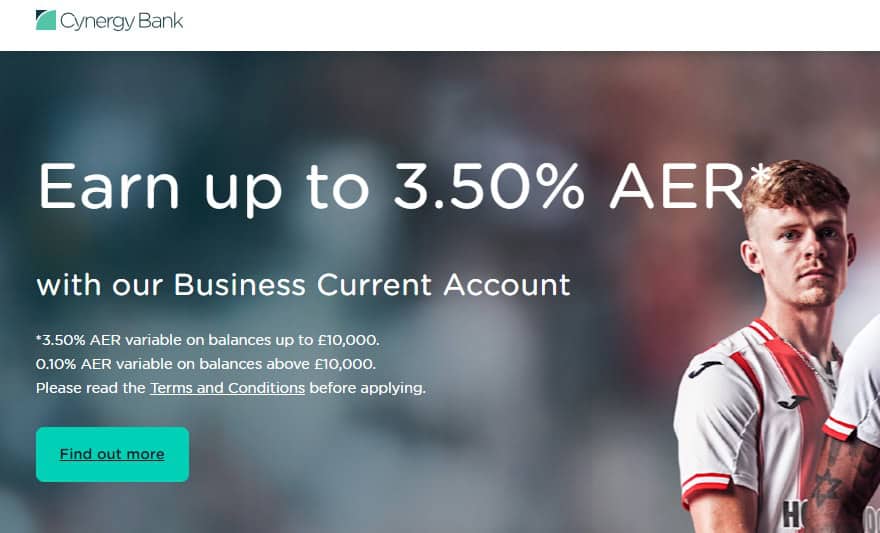

| Cynergy Bank | 3.50% | 3.50% |

| Virgin Money | 1.10% | 3.50% |

| Wise* | 1.75% | 3.41% |

| Shawbrook Bank | 3.40% | 3.40% |

| Revolut* | 2.15% | 3.30% |

| Charity Bank | 2.94% | 2.94% |

| Allica Bank | 2.80% | 2.80% |

| Cumberland Building Society | 2.20% | 2.40% |

| Aldermore | 2.45% | 2.45% |

| OakNorth | 2.35% | 2.35% |

| Dudley Building Society | 3.75% | 3.75% |

| Saffron Building Society | 1.20% | 3.30% |

| Recognise Bank | 3.15% | 3.15% |

| Cambridge Building Society | 1.55% | 1.55% |

| ICICI Bank UK | 1.60% | 1.60% |

| Unity Trust | 2.77% | 2.77% |

| Allied Irish Bank | 0.25% | 0.25% |

| Nationwide | 0.00% | 1.50% |

| State Bank of India | 0.00% | 1.55% |

| Barclays | 1.05% | 1.51% |

| NatWest | 0.85% | 1.46% |

| RBS | 0.85% | 1.46% |

| HSBC | 1.21% | 1.31% |

| Monzo | 1.30% | 1.30% |

| Lloyds Bank | 0.50% | 1.21% |

| Bank of Scotland | 0.50% | 1.21% |

| Ulster Bank | 0.85% | 1.46% |

| Danske Bank UK | 1.65% | 1.65% |

| Co-operative Bank | 1.06% | 1.06% |

| TSB | 1.35% | 1.50% |

| Santander | 0.40% | 1.00% |

| Mettle | 1.46% | 1.46% |

| Metro Bank | 0.85% | 0.85% |

* Note Wise, Tide & Revolut are not banks but e-money institutions. Data accurate at the time of publication but may have since changed.

1. Wise

- Earn returns on GBP, USD and EUR by opening a Wise account and investing in a fund that holds government-guaranteed assets.

- Spend any time

- Growth is not guaranteed and your money is at risk if governments default or interest rates go negative. Variable rates are based on 7 day performance as of 19/03/2024.

- Interest is offered in partnership with BlackRock and through Wise Assets. The funds aim to maximise current income through a portfolio of high quality short-term money market instruments.

- You may have to pay tax on your earnings — for example, capital gains tax.

- Rates shown are after fees.

- You may also be eligible for protection up to £85,000 under the Financial Services Compensation Scheme (FSCS).

- Returns are added every working day

See more on the Wise website.

2. Tide

- Interest, paid monthly on savings

- Flexible, easy access to savings

- No limits or fees on withdrawals

- Deposit as little as £1

- Eligible deposits with ClearBank are protected up to a total of £85,000 by the Financial Services Compensation Scheme (FSCS)

- Track everything in app

See more on the Tide website.

3. Shawbrook Bank

- Min balance: £1,000

- Max balance: £85,000

- Take out money whenever you like, as long as the amount is at least £500.

- You’ll receive your money within one working day if you withdraw before 9:30pm

- Available to sole traders, a limited companies (limited by shares) or partnerships (excluding limited liability partnerships)

- Need four or less signatories authorised to operate the account

- If your balance drops below £1,000 interest your rate will change to 0.05%.

- You can only open this account online.

- Eligible deposits are protected up to a total of £85,000.

- This account is not available to charities or trusts

For more visit Shawbrook Bank website.

4. Allica Bank

- Flexible saving. Withdraw anytime.

- Apply online

- Eligible deposits are covered by the FSCS up to £85k.

- Interest is calculated daily and paid annually

- You can invest between £20,000 and £100,000 into the account

- If account balance falls below £20,000 they may close your account

- Must be a UK business registered with Companies House

For more visit Allica Bank website.

5. Cynergy Bank

- Start saving from just £1.

- Make unlimited requests to withdraw your money at any time.

- Eligible deposits are protected up to £85,000.

- Available to sole traders, partnerships, limited liability partnerships and limited companies.

- Open an account in as little as 10 minutes with their online application process.

- Business Saver enables up to 10 directors as signatories

- Businesses based in the UK and registered with Companies House

- No Charities, trusts, clubs or societies.

- Not available if any signatory is a US citizen

For more visit the Cynergy Bank website.

6. OakNorth

- Get access to interest-bearing savings automatically when you open a current account.

- Move money easily between your current account and savings

- Access your savings, plus accrued interest in one-working day

- You can only access your Earn Vault via the mobile app

- No minimum or maximum deposit limits apply to your Earn Vault

- If they receive your withdrawal request on a business day before 8am, they will move the money to your current account on the same day.

- If your request is received on a business day after 8am, they will move the money to your current account on the next business day.

- Currently on waiting list

For more visit the OakNorth website.

7. Virgin Money

Virgin Money offers two Instant Access accounts: Business Cash Management Account and Business Access Savings Account. As the Business Access Savings Account offers far better interest rates the below applies to that account:

- Save from £1 up to £2 million with monthly interest

- Monthly interest is paid on the 10th of each month, and will be available the next business day

- Operated separately from your Business Current Account

- No Fees and Charges

- Top up or access your savings instantly whenever you like

- This is a standalone online account and is serviced using Online Service.

- This account doesn’t link with your Business Current Account, Business Internet Banking or our mobile app

- Electronic transfer to your nominated business account only.

- Minimum withdrawal amount £1

- A maximum of two account signatories can be on the account.

- Available to sole traders, partnerships, limited liability partnerships, private limited companies or a public limited companies

- Your business is classed as a micro, small or medium enterprise (SME)

For more visit the Virgin Money website.

8. Dudley Building Society

- Minimum opening and operating balance: £1,000

- Maximum operating balance: £1,000,000

- Instant access withdrawals are permitted with this account

- Interest is paid annually on the 31st March.

- This account is available for Corporate Bodies

- Any queries regarding your account can be dealt with via branch, email or telephone. Instructions on operating your account are required in person, at branch or in writing.

- You may open your account at any one of one of their branches or via post.

For more visit the Dudley Building Society website.

9. Aldermore

- Minimum opening balance: £1,000

- Apply online at whatever time of day works for you.

- You can access your money whenever you need it

- Your money is protected up to £85,000 by the Financial Services Compensation Scheme.

- Customers have rated them “excellent” on Trustpilot.

- Awarded Best Variable Rate Business Savings Provider by Moneynet in 2024

- You can close your account at any time without notice or penalties.

- Don’t provide accounts for limited partnerships, limited liability partnerships, partnership, sole trader, clubs, societies or charities)

- Your business must only tax resident in the UK

- Interest calculated daily, and paid monthly or annually.

- You can’t be a US citizen

For more visit the Aldermore website.

10. Revolut

- Interest paid daily (including weekends) directly to your Business account

- Add or withdraw money with zero restrictions

- Set controls for who else gets access

- Savings are deposited with their trusted partner banks and are protected by the Financial Services Compensation Scheme (FSCS) up to £85,000.

- Save up to £2,000,000 on their Enterprise plan (which also offers the highest interest rate)

- Savings is available for all Businesses on Grow (£19/month), Scale (£79/month), and Enterprise plans (bespoke pricing)

- Must have annual turnover of £36M or less

For more visit the Revolut Business website here.

11. Saffron Building Society

- Online, instant access savings account

- Need a minimum deposit of £10,000

- You’ll need to keep a minimum balance of £10,000.00 in your account to get the interest rate.

- You must be a limited company, limited partnership, limited liability partnership or charity registered in the UK

- You must be a UK resident aged 16+

- Interest is calculated each day on the available money in your account and is paid on 31 December every year.

- Can manage the account online and on the mobile app.

For more visit the Saffron Building Society website.

12. Cumberland Building Society

The Cumberland Building Society offers two instant access accounts Instant Access and eSavings. Below we focus on their eSavings offering as it pays the higher interest rate.

- Minimum balance: £1

- Interest is calculated on a daily basis, and is paid gross (without deduction of tax) annually on 31 March to your Cumberland Business current account.

- Only open to existing customers who live within their branch operating area.

- Instant access withdrawal via online transfer to your Cumberland business current account.

- This account is not available to schools.

- An exclusive online savings account available to Business Internet Banking customers.

- Withdrawals not permitted by direct debit, standing order, regular internal transfer or faster payments.

For more visit the Cumberland Building Society website

13. Recognise Bank

- Min balance: £1,000

- Max balance: £250,000 (For Limited Companies and Limited Liability Partnerships)

- Max Balance: £85,000 (For Sole Traders or Partnerships)

- Open an account in minutes, for free

- Complete control and competitive rates

- Up to 4 people in your business can manage your account

- Interest is calculated daily.

- You can choose to have your interest paid monthly or annually

- To open an Account you must be: a Small to Medium Enterprise with fewer than 250 employees and either assets of less

than £36.5 million and/or turnover of less than £42.5million - All deposits are protected up to £85,000

For more visit the Recognise Bank website.

14. Cambridge Building Society

- Your interest will be paid annually, on the 31st December.

- Minimum investment: £1,000+

- Max Investment: £2,500,000

- Open in branch or via post. Your account must be opened with a cheque from your business bank account

- Available to Sole Proprietors, Partnerships, Limited Companies, Public Limited Companies, registered Charities, Housing Associations, Clubs and Associations

- Pay in up to £1,000 in cash (notes only) and one cheque per day

- Make debit card payments at any of our branches or over the phone

- You can view and amend your details online or via The Cambridge money app. Once registered you can also use our online services to manage your account

- You can withdraw cleared funds from your account, up to twice a month, without giving notice or paying a fee. Normal branch limits for withdrawals are £500 in cash and up to £250,000 by cheque. Larger cheque withdrawals are available upon request.

- Covered by the Financial Services Compensation Scheme (FSCS)

For more visit the Cambridge Building Society website.

15. ICICI Bank UK

- Start from £1

- Max savings up to £5m

- Need to hold a Business Current Account with ICICI Bank UK

- Customers can make penalty-free withdrawals in the form of transfers to their ICICI Bank UK Business Current Account

- No notice period is required for withdrawals

For more see the ICICI Bank UK website

16. Unity Trust

- Minimum deposit: None

- Maximum Deposit: None

- Variable access with no notice of withdrawal required

- Your money is FSCS protected, up to £85,000

- Interest will accrue daily on the amount of Funds deposited in the Account and subject to any Withdrawal is compounded quarterly,

interest is capitalised on the Funds deposited quarterly in March, June, September and December. - To open an account, you must be a UK-based organisation.

For more see the Unity Trust website

17. Allied Irish Bank

- There are no minimum or maximum limits to depositing into this account.

- Interest is calculated and accrued daily based on the balance in your account. Interest will be

credited to your account annually at the beginning of April. - No transaction charges

- You can open a Demand Deposit Account by calling them on 0345 6005 204

- You can manage your account through Online Banking or over the phone.

- You can withdraw funds: Via Online Banking and Phoneline Banking or By sending a signed written instruction to Allied Irish Bank (GB) 92 Ann Street, Belfast, BT1 3HH.

For more see the Allied Irish Bank website

18. Nationwide

- You can choose to have your interest paid monthly or annually. Interest is calculated daily.

- Business Savings account are covered by the Financial Services Compensation Scheme

- If your balance falls below £5,000 you will not earn interest until your balance returns to £5,000 or more.

- The following organisations can open an account: Limited companies, Charities, Partnerships, Sole Traders, Housing Associations, Clubs & Societies, Parish Councils

- Organisations that can’t open an account: Banks/Building Societies, Insurance Companies, Corporate Trust, Borough Councils, Cash/Liquidity Fund, Company Pension, Friendly Society, Life Policy, Investment and Unit Trusts and Government/Political Parties

- Must have annual turnover of less than £10 million

- You can only open our Business Savings accounts by applying online

- Current timescales to process applications are 12 weeks.

For more see the Nationwide website

19. State Bank of India

- No annual fee with minimum monthly average balance.

- Available only for micro-enterprise, which are incorporated in the European Economic Area (EEA). A Micro-enterprise is a business that employs fewer than 10 persons and has a turnover or annual balance sheet that does not exceed €2mn.

- For GBP Business Savings Account, if the minimum balance of £10,000 is maintained, you can make up to 25 free transactions each month, after which standard charges apply.

- Interest is paid on the last working day of the month.

- Interest will not be paid on balances below £10,000 for all GBP accounts and below $100,000 for all USD accounts.

- Account can be managed in the branch, by post or by using the online banking facility provided with the account.

For more see the State Bank of India website

20. HSBC

- There are no minimum or maximum deposit amounts.

- Instant access to your money, whenever you need it

- Interest is calculated daily, and paid monthly

- Apply in the HSBC Kinetic mobile app in minutes

- No monthly fees

- You are eligible if your business has annual turnover of up to £6.5 million.

- You do not need to open, hold or maintain an account with HSBC to open this account.

- You can make as many withdrawals as you like in cash in branch or by making an electronic payment to your HSBC Kinetic Current Account if you have one or, if you don’t, your nominated account in the same name.

- You don’t have to give us any notice, but if you take money out of your account, your interest rate may change.

For more visit the HSBC website

21. Barclays

- Minimum balance: £0

- Maximum balance: £50 million

- Manage Online, branch, phone

- Interest is calculated daily using your statement balance and is paid quarterly in March, June, September and December.

- Unlimited free withdrawals via your Business current account

- Make unlimited CHAPS payments, also known as ‘same-day domestic payments’ (standard charges apply)

- Open your account by speaking to their telephone servicing team or with one of their Business Managers in one of their branches.

For more visit the Barclays website

22. NatWest

- No minimum or maximum balance

- Instant access to funds – no notice of withdrawal required

- You can apply for a Business Reserve instant access account if you have a business registered in England, Scotland, or Wales.

- No penalties for withdrawal

- Account management available online or by telephone banking

- Interest calculated daily and applied monthly

- Interest rate is not directly linked to Bank of England base rate

- They review interest rates regularly and may change them from time to time (60 days notice given)

For more see the Natwest website

23. Lloyds Bank

- £1 minimum deposit

- Application should only take about 10 minutes

- Interest is calculated daily and paid monthly.

- This account can be opened and managed by phone or online.

- You can make withdrawals from this account and there are no charges for doing so.

- You can close this account at any time.

For more visit the Lloyds Bank website

24. Bank of Scotland

- Start saving from as little as £1

- Instant access to your savings

- Interest calculated daily and applied monthly

- Make unlimited withdrawals and pay in additional fund

- Eligible deposits with Bank of Scotland plc are protected up to a total of £85,000. Due to FSCS eligibility criteria not all business customers will be covered.

For more visit the Bank of Scotland website.

25. RBS

- There is no minimum deposit required to open the account, and there is no maximum balance limit.

- Earn interest daily on your savings and receive it on the last business day of every month

- Access to your business savings instantly

- Make as many withdrawals as you need without penalties

- You can withdraw money:

- in branch.

- by transfer to your business current account at Royal Bank of Scotland

(in branch, online, by telephone or on the mobile app). - by transfer to any other account based in the UK (online, by telephone or on the

mobile app).

For more see the RBS website

26. Ulster Bank

- No minimum or maximum balance

- Interest is calculated daily and paid monthly

- Instant access to funds

- No limit to the number of withdrawals

- Single rate of interest on entire balance

- No penalties for withdrawals

- Your eligible deposits with Ulster Bank are protected up to a total of £85,000 by the Financial Services Compensation Scheme, the UK’s deposit guarantee scheme.

For more see the Ultser Bank website

27. Danske Bank UK

- The minimum amount required to open and maintain an account is £1.

- You can save as much as you like.

- Interest is calculated daily and applied quarterly to your account.

- There is no debit card available with this account.

- You can have more than one account.

- When you need to make a withdrawal simply transfer what you need to your main business account. There is no notice period or penalty for withdrawals.

- You can access your funds 24/7 using District.

For more see the Danske Bank UK website

28. Co-operative Bank

- Interest is calculated daily and will be paid into your account on 5 April and 5 October.

- No minimum or maximum account balance required

- Easy, same-day access to funds

- Only existing customers can apply online

- You can make withdrawals through online or telephone banking to your linked Co-operative Bank business current account.

For more visit the Co-operative bank website

29. Monzo

- Interest paid monthly

- No minimum deposit

- If you’re a sole trader or a small business your eligible deposits may be protected by the Financial Services Compensation Scheme (FSCS) up to £85,000 per person.

- Access and withdraw anytime, no restrictions

- App lets you keep your savings separate from your tax funds and balance

For more visit the Monzo website

30. TSB

- Open an account from just £1

- Interest calculated daily and paid monthly.

- No penalties for withdrawals

- No limits or fees

- You don’t need to be an existing TSB customer to apply

- Apply online

- Lower rate of interest on balances below £5,000

- Manage your account online 24/7 with TSB Internet Banking or the TSB Business Mobile Banking App

- Can also visit them in branch

For more see the TSB website

31. Santander

Santander offers two instant access accounts: Business Everyday Saver and Business Reward Saver. We’ve focused on the Reward Saver account as it offers a slightly higher rate of interest.

- Minimum opening deposit of £1

- No maximum balance.

- Interest paid each month into the account on the anniversary of the date it was opened.

- Easy access through online, phone and cash machine

- A lower rate of interest when you make a withdrawal

- Instant access using Online Banking, and on the move with their Mobile Banking app, Telephone Banking and with a cash card

- You can have up to two directors, owners (shareholders) or partners

- You’re either a sole trader or your business is a partnership, limited liability partnership or a private limited company

- The Business Reward Saver converts to the Business Everyday Saver account after 12 months

For more see the Santander website

32. Mettle

- Earn on balances from as little as £10.

- You can set aside up to £1 million in your savings pot

- Need to have an exiting Mettle Business Account to apply

For more visit the Mettle website

33. Metro Bank

- No minimum deposits

- Interest paid monthly or annually

- Easy access to your cash

- No hidden fees

- You won’t pay a monthly fee

- There are no set-up costs

- To open a Business Instant Access Deposit account, you need: To be 18 or over, At least 50% of the business’s directors or beneficial owners (people who own more than 25% of the shares) are residents in the UK and At least 50% of shares owned by UK residents

- You can manage your Business Instant Access Deposit Account online or on your mobile.

For more see the Metro Bank website

Which bank offers the highest interest rate on business savings?

Wise is currently offering the highest interest rate on instant access business savings at 4.66%. However, they are not actually a bank but an e-money institution. And they are not really offering a normal business savings account. Instead you are investing in a fund that holds government-guaranteed assets.

According to them:

Interest is offered in partnership with BlackRock and through Wise Assets. The funds aim to maximise current income through a portfolio of high quality short-term money market instruments. You may have to pay tax on your earnings — for example, capital gains tax.

Tide offers the next highest interest rate at 4.33% AER. But Tide is also not a bank.

However, their eligible deposits are held with ClearBank, who offer protection up to a total of £85,000 by the Financial Services Compensation Scheme.

So their product is more or less the same as normal bank backed savings account, but with slightly more risk. Your money may not be fully protected when in-transit and you may not benefit from the full FSCS protection if your business holds other accounts at ClearBank.

Therefore, in terms of actual banks Shawbrook Bank, Allica Bank and Cynergy Bank are the only ones to offer savings accounts paying interest at or above 4.00% AER.

Which high-street bank offers the highest interest rate on business savings?

Honestly, all the of the UK’s high-street banks offer low business savings rates. Virgin Money has an a standalone Business Access Savings Account that currently pays 3.80% AER, but their standard Business Cash Management Account only pays 1.35% AER.

In terms of the biggest high-street banks here is what they pay:

- HSBC: 1.93% – 1.96% AER

- Barclays: 1.51% – 1.96% AER

- NatWest: 1.46% – 1.92% AER

- Lloyds: 1.31% – 1.92% AER

Which bank offers the worst business savings rates?

Metro Bank currently offers the lowest standard interest rate on their business savings at just 1.20% AER. However, they only have a £1 minimum balance so you should at least get paid something on your business savings.

The following banks actually offer even lower rates in certain situations:

- Santander’s Business Reward Saver interest rate drops to 0.40% AER in any month you make a withdrawal.

- Shawbrook’s Easy Access Business Account interest rate falls to 0.05% AER if your account balance falls below £1,000.

- Nationwide will not pay you any interest if your account balance falls below £5,000.

- State Bank Of India will not pay any interest on your account if your balance falls below £10,000.

And of course, virtually all current accounts in the UK pay no interest at all, so even 1.20% is better than that.

Are instant access business savings rates fixed or variable?

All instant access business savings accounts in the UK offer variable interest rates, not fixed.

This means your bank can change your interest rate at anytime, often at relatively short notice.

However, most banks also offer fixed interest products such a notice accounts and corporate bonds if you want a product with more stability and/or predictability.

Can my bank change my interest rate?

Yes, as stated above your bank can change your business savings rate. Common reasons to do so include the following:

- Change in the Bank of England Official Base Rate (currently 5.25%)

- Change in market conditions for your bank

- Change in government regulation and/or legislation

You should carefully read your bank’s terms and conditions to understand how much notice they have to give you before changes come into effect.

Does the interest rate paid on business savings really matter?

The table below compares how much more money you’d have after a year with Tide (bank offering the highest instant access interest rates) compared to Metro Bank (the one currently offering the lowest rate).

| Initial Deposit Amount | Tide Total With Interest (4.33%) After 1 Year | Metro Total With Interest (1.20%) After 1 Year | How Much Extra You'd Have |

|---|---|---|---|

| £1,000 | £1,043.30 | £1,012.00 | £31.30 |

| £10,000 | £10,433.00 | £10,120.00 | £313.00 |

| £100,000 | £104,330.00 | £101,200.00 | £3,130.00 |

| £1,000,000 | £1,043,300.00 | £1,012,000.00 | £31,300.00 |

| £10,000,000 | £10,433,000.00 | £10,120,000.00 | £313,000.00 |

On smaller amounts the differences are quite small, but start to really add up as your deposits grow.

Are business savings accounts in the UK protected?

Yes, business savings accounts in the UK are protected under the Financial Services Compensation Scheme (FSCS). The FSCS provides a safety net for individuals and small businesses when authorized financial services firms fail.

Specifically, the FSCS covers:

- Deposits up to £85,000 per eligible business, per financial institution: This means that if a bank or building society fails, the FSCS will compensate the business up to this limit. If the business has more than £85,000 deposited in a single financial institution, any amount over this threshold would not be protected.

- Joint accounts: For joint accounts held by businesses, the FSCS protection limit is £85,000 per person, so a joint account could be covered for up to £170,000.

It’s important for businesses to ensure that their bank or financial institution is authorized by the UK’s Prudential Regulation Authority (PRA) and that they qualify under the FSCS criteria to be eligible for this protection.

Larger businesses, or those classified outside of the small business criteria (typically those having an annual turnover of more than £1 million), may not be eligible for FSCS protection. Thus, they should check their eligibility and possibly spread their risk by keeping funds in different financial institutions if necessary.

How to open an instant access business savings account?

Opening a business savings account in the UK involves several steps and requires gathering specific documents to meet regulatory and bank-specific requirements. Here’s a general guide on how to proceed:

1. Choose the Right Account

- Research Options: Different banks offer various features, interest rates, and terms on their business savings accounts. Consider what’s most important for your business, such as accessibility, interest rates, and transaction fees.

- Comparison: Use financial comparison websites to compare different savings accounts available in the UK to find one that best suits your business needs.

2. Prepare Necessary Documentation

To open a business savings account, you will generally need the following documents:

- Proof of Identity and Address for Key Individuals: Such as directors and significant shareholders. Typically, a passport, driving license, or national ID can serve as proof of identity. Utility bills or bank statements (dated within the last three months) can be used as proof of address.

- Business Documents:

- Certificate of Incorporation

- Memorandum and Articles of Association

- Details of your business’s structure and management

- Recent business bank statements (if applicable)

- Proof of business address (e.g., utility bill or lease agreement)

- Details of All Directors and Beneficial Owners: This is part of the bank’s Know Your Customer (KYC) compliance.

3. Apply Online or In-Person

- Online Application: Many banks offer the convenience of applying online. This process typically involves filling out an application form and uploading digital copies of your documents.

- In-Person Application: You may also visit a bank branch to open an account, which can be beneficial if you have specific questions or unique business circumstances. It may also be necessary for businesses with complex structures or for banks that require in-person verification.

4. Initial Deposit

- Some banks may require an initial deposit to open the account. Check the requirements of the specific bank regarding minimum deposit amounts.

5. Wait for Approval

- After submitting your application and documents, the bank will review them for compliance with financial regulations. This process can take anywhere from a few days to a few weeks.

6. Set Up Account Features

- Once your account is opened, set up any additional features such as online banking, mobile alerts, or standing orders according to your business needs.

7. Maintain the Account

- Monitor your account regularly, manage deposits, and keep track of interest earnings and any applicable fees.

Tips:

- Check Eligibility: Ensure your business is eligible for the account type you choose.

- Understand Fees and Terms: Be clear about any fees for maintenance, transactions, or early withdrawals, as well as how interest is calculated and paid.

- Consider Multiple Accounts: If you have substantial savings, consider spreading them across different accounts to maximize FSCS protection.

What else can you do with business savings besides opening a business savings account?

Here are some of the options available (note most of these involve more risk than simply holding cash in a business savings account):

- Invest in Stocks and Shares: The UK stock market offers opportunities for businesses to invest their surplus funds. Investing in individual stocks or diversified ETFs can yield higher returns compared to traditional savings, though it comes with higher risk.

- Bonds and Fixed-Income Securities: Corporate and government bonds can be a safer investment alternative to stocks. They provide a fixed return over a period and are generally considered lower risk than equities.

- Money Market Funds: These are excellent for businesses that require both a reasonable rate of return and liquidity. Money market funds invest in short-term debt securities and typically offer higher interest rates than savings accounts.

- Real Estate Investment: The UK’s real estate market can be a lucrative area for investment. Whether through direct property purchases or real estate investment trusts (REITs), real estate can provide both rental yields and capital appreciation.

- Peer-to-Peer Lending: This has become a popular way for businesses in the UK to invest surplus funds. By lending money to other individuals or businesses through a peer-to-peer platform, businesses can earn interest rates that often surpass those of traditional savings accounts.

- Venture Capital/Angel Investing: For businesses with a higher risk tolerance, investing in startups or becoming angel investors can offer substantial returns if the enterprises grow significantly. This is more common among businesses that have substantial excess funds and a strategic interest in fostering innovation within their industry.

- Pay Down Debt: Utilizing excess funds to reduce debt, especially high-interest debt, can improve the business’s net financial position and reduce ongoing interest costs.

- Expand Operations or Upgrade Technology: Reinvesting funds into the business for expansion, technology upgrades, or research and development can drive growth and efficiency, providing long-term financial benefits.

- Specialized Business Accounts: Consider investing in specialized business accounts that offer benefits for holding larger balances, such as tiered interest rates that increase with the account balance or accounts that blend the features of both savings and checking accounts.

- Corporate Bonds and Gilt Funds: Investment in UK government securities (gilts) or corporate bonds can be a more conservative investment strategy that still offers returns above those typical of savings accounts.

- Corporate Social Responsibility (CSR) Projects: Investing in CSR activities can not only fulfill ethical obligations but also enhance the company’s brand reputation and customer loyalty, potentially leading to increased profitability.